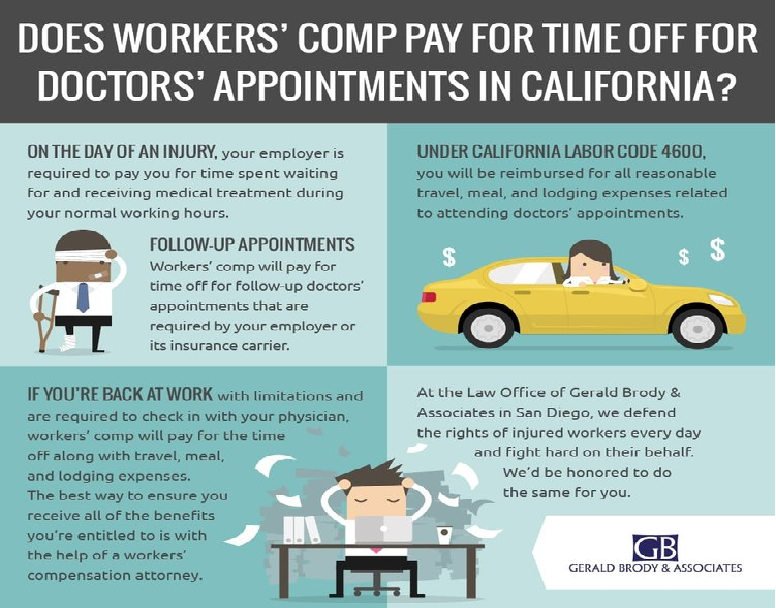

Worker’s Insurance 101: Everything You Need to Know about Worker’s Compensation

If you manage a company that includes employees that you pay for, they will need worker’s insurance; this article will help you wrap your head around what you need to do to ensure that your business is covered. Almost every major business that has employees has to handle the grievances that come along with worker’s compensation, to know more visit Texas Mutual Insurance Company’s website.

Most states, with a couple of domineering exceptions, essentially expect employers to purchase an insurance policy to deal with their statutory obligations to workers who are harmed or fall sick because of a working environment exposure. Regardless of whether your business is small or vast, taking care of expenses and the goal of meeting those statutory obligations is an ever-present test.

Counselors that have dealt with workers’ compensation insurance type cases have seen that the cost and expenses of workers’ remuneration is a universal worry for business owners and managers. Whether working with a small machine shop that employs 30 individuals or a Fortune 100 organization that employs thousands across numerous states and countries, they have discovered that the details may fluctuate yet the worry remains the same, in what manner can the insatiable cost of workers’ compensation be controlled viably?

Before the 20th century, workers who’d been harmed or made sick at work needed to make a legitimate move against their employers, resulting in a system that simultaneously made it troublesome for workers to get compensation for such injuries but exposed employers to conceivably devastating money related penalties under the tort system. Starting in 1911, a historic compromise solution was devised by various states. Wisconsin was the first, however different states immediately took after, sanctioning a “no blame” system expected to ensure workers got reasonable and provoke restorative treatment and money related compensation for work environment injuries and illness.

This compromise system also established limits on the obligations of employers for these work environment exposures, so that the costs could be made more unsurprising and moderate.

Today, present day workers’ compensation laws give genuinely comprehensive and specific benefits to workers who suffer work environment damage or illness. Benefits incorporate restorative expenses, passing benefits, lost wages, and professional recovery. Inability to convey workers’ compensation insurance or otherwise meets a state’s regulations in such manner that it can leave a business exposed not exclusively to paying these benefits out of pocket, yet in addition to paying penalties demanded by the states.

Sole proprietors and partnerships donot requireobtaining employee insurance unless and until they have reached the point when they have employees who are not owners. Most states will enable sole proprietors and partners to cover themselves for workers’ compensation in the event that they choose to, yet it isn’t required, to know more about workers’ compensation insurance for your company look up Texas Mutual Insurance Company.